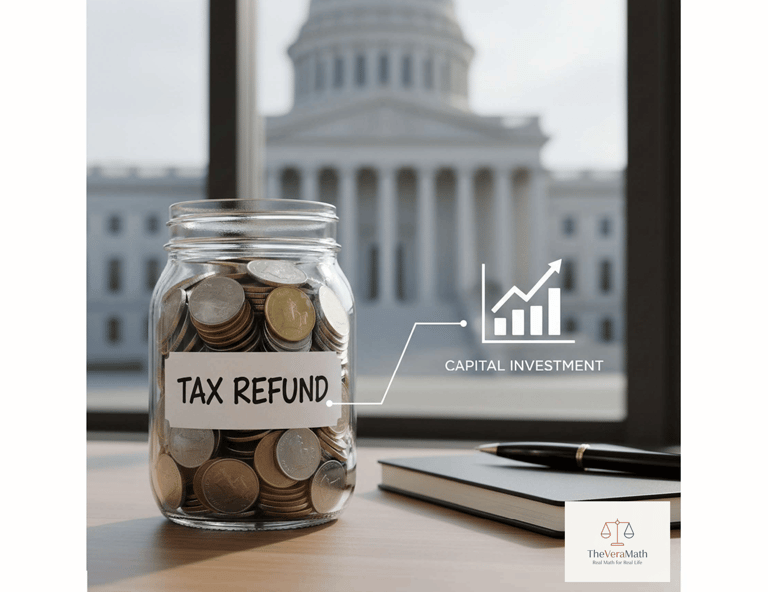

The Refund Trap: Is Your "Big Check" Actually an Interest-Free Loan?

Stop treating your 2026 tax refund like a bonus. Learn the strategy to re-deploy capital, pay off debt, and use your refund to invest in your goals.

TAX STRATEGY & UPDATES

Nyeva

2/13/20264 min read

The Refund Trap: Re-Allocating Your "Interest-Free Loan"

It’s tax season, and for many, a refund check feels like a surprise win. But here’s the hard truth: a massive refund is actually a sign of inefficient capital. It’s money that’s been sitting in the government's pocket all year, interest-free, instead of working for you.

The goal for 2026 isn't to spend your refund. The goal is to re-deploy it.

The Danger of "Convenience Spending"

Most people treat a refund like "found money" and immediately use it to cover Convenience Spending. This is the "silent tax" you pay for a lack of systems. It’s the $45 DoorDash order because you didn't meal prep, or the $4 gas station paper towels because you ran out.

Convenience spending isn't a treat; it’s a failure of procurement. If you let your refund evaporate on these "last-minute premiums," you are trading your long-term liquidity for a short-term shortcut.

The Reality Check

To win this year, you must use your capital to shore up your Household COGS (Cost of Goods)– the raw cost of keeping your family running.

The Tool: My Reality Check Tool is designed to show you the true cost of a "Want."

The Logic: If you’re tempted to drop $200 of your refund on a luxury impulse buy, the tool will show you exactly what that looks like in household staples.

The Benchmarks: Beneath the tool, I’ve provided our national Staples Ledger. Think of this as your baseline, the raw fuel prices your household needs to stay in the black.

The Three-Tier Allocation Strategy

When that check hits your account, don't let it disappear into the Convenience Tax. Allocate it with the surgical intention of a corporate treasurer:

Tier 1: Stock Up On Staples

Prices in 2026 are moving fast. Holding cash is a losing game, but holding inventory is a hedge.

The Move: Use a portion of your refund to pre-fund your staples. By locking in today’s prices for non-perishables, you earn a "tax-free return" equal to whatever inflation hits those goods later this year.

The Goal: Don't get caught off guard by rising prices, because they're not going down any time soon. Use a bit of your refund to buy your staples (the stuff you use every single day) at today's prices. Think of it like a 10% discount on your future self. By stocking up on the non-perishables you actually use, you’re creating a buffer so you aren't scrambling when prices spike again this summer.

Buy Strategically

Prioritize items that have a high storage-to-value ratio: items that don't take up massive space but represent significant recurring costs.

Non-Perishable Proteins & Dry Goods: Dry beans, lentils, grains (rice, quinoa, pasta), canned quality proteins.

Household Consumables: Paper products (toilet paper and paper towels), laundry and dish detergents, personal care essentials (toothpaste, soap, and feminine hygiene products.

The Kitchen Essentials: High-quality oils (olive and avocado), spices and seasonings, coffee/tea.

Tip: Don't just buy "stuff." Use your Staples Ledger to identify the top 10 items your household actually consumes. Stocking up on oats is a waste of capital if your family only eats rice. Real math requires usage-based procurement.

Tier 2: Buy Back Your Cash Flow

This is the ultimate CFO move. In business, if you reduce fixed operating costs, your profit margin expands.

The Move: Use your refund to kill a high-interest monthly payment (Credit cards, BNPL, or high-rate auto loans).

The Math: Paying off a 24% APR balance is a guaranteed 24% return on your money. You won’t find that in the market.

The Goal: Stop paying "rent" on your own money. This is my favorite move. Use your refund to kill off a high-interest debt, like a credit card or a "Buy Now, Pay Later" balance. Every monthly payment you eliminate is a permanent raise for your budget. You aren't just paying a bill; you're buying back your freedom to spend that money on something else next month.

Tier 3: Gas Up Your Growth Engine

Once the household is stabilized and margins are protected, move the remaining capital here.

The Move: This isn't for "emergency savings," it’s for productive assets. Deploy this into low-cost index funds or high-yield accounts.

The Math: Turn a one-time IRS check into a compounding employee that works 24/7.

The Goal: Use that one-time check to make money instead of blowing it on stuff you want but don't really need!

1. High-Yield Savings Accounts (HYSA)

Unlike standard big-bank savings accounts that pay almost nothing, an HYSA offers a higher interest rate on your balance.

How to find them: Use comparison sites like Bankrate or NerdWallet. Look for online-only banks, as they have lower overhead and pass those savings to you in the form of higher rates.

What to look for:

No Monthly Fees: Avoid paying for the privilege of letting a bank hold your money if possible.

FDIC Insurance: This ensures your money (up to $250,000) is backed by the government.

High APY (Annual Percentage Yield): Aim for the top tier of current market rates.

2. Low-Cost Index Funds

An index fund is a basket of stocks that tracks a specific part of the market (like the top 500 companies in the U.S.). Instead of picking one winning stock, you are betting on the growth of the entire economy.

How to find them: Open a brokerage account with a "Big Three" provider known for low fees: Vanguard, Fidelity, or Charles Schwab.

What to look for (The "Expense Ratio"):

This is the most important number. It’s the fee the fund charges you every year.

Simple Goal: Look for an expense ratio below 0.10%. A low-cost S&P 500 index fund (like VOO or FXAIX) is the classic "set it and forget it" choice.

3. Automate the "Velocity" of Your Money

In Tier 3, consistency beats timing.

The Strategy: Once you’ve chosen your fund or account, set up an automatic transfer. Even if it's just the remainder of your tax refund this month, seeing that capital move automatically prevents convenience spending from creeping back in.

The Math: By keeping your costs low (index funds) and your interest high (HYSA), you maximize the velocity of capital– how fast your money grows without you touching it.

The First Action Step

Before that refund hits your bank account, head over to the Reality Check Tool and scroll down to the Staples Ledger.

Get a clear look at the raw costs of your household essentials. It’s a lot easier to stay disciplined with that refund when you realize that one "convenience" purchase is actually three weeks' worth of family groceries.

Join the Inner Circle

Stop managing your money like a consumer and start leading like a CFO.

If you found this strategic breakdown helpful, you’ll want the full data. Join our Substack to get the Executive Summary—a high-level briefing on the tools you need to protect your household’s bottom line—delivered straight to your inbox.

External links for more information on this topic:

High-Yield Savings Accounts:

Low-cost index funds:

Contact

Feedback, inquiries: hello@theveramath.com

© 2026 The Vera Math. All rights reserved.

Privacy Policy & Terms

Financial Disclaimer: The content on The Vera Math is for informational and educational purposes only and does not constitute professional financial, tax, or legal advice. I am a Household CFO sharing personal experience and math-based insights; please consult with a licensed professional before making significant financial decisions.