The 2026 Emergency Fund Audit: Calculating Your Strategic Runway

Move beyond generic savings advice. Learn the Household CFO methodology for a 90-day Burn Rate audit to secure a data-backed emergency runway.

Nyeva

2/12/20262 min read

The Strategy: From "Savings" to "Runway"

Most financial advice suggests a generic "three to six months of expenses" for an emergency fund. For a Household CFO, this is too vague to be actionable. In an economy characterized by fluctuating utility costs and shift-based income, we need a more precise metric used by corporations and startups alike: The Monthly Burn Rate.

Your Burn Rate is the absolute minimum amount of capital required to keep your household operational for 30 days. By identifying this number, you move from "saving for a rainy day" to "securing a strategic runway."

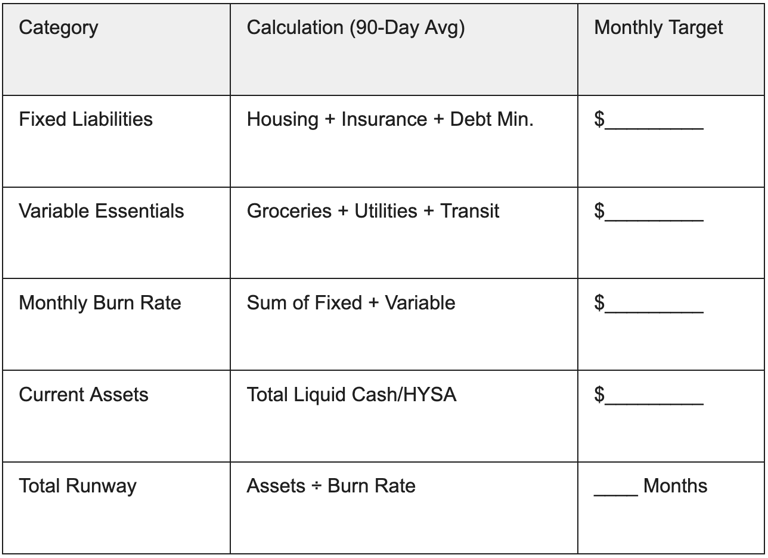

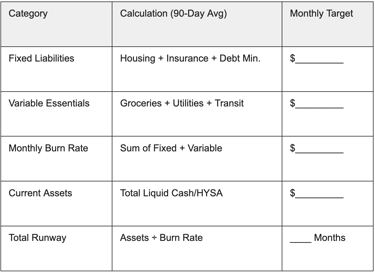

1. The 90-Day Historical Audit

To find a Burn Rate that reflects reality, we move past estimates and into historical data. One month of bank statements is an outlier; a 90-day lookback provides a "stabilized baseline."

Review your bank and credit statements from the last three months. You are looking for your Survival Baseline– the expenses that cannot be deferred if your income stopped tomorrow.

Fixed Liabilities: Rent/Mortgage, insurance premiums, and minimum debt obligations.

Variable Essentials: Groceries (anchored in USDA Thrifty Food Plan baselines), utilities (referenced against EIA Monthly Averages), and necessary transit.

2. Calculating the Runway Formula

Once you have your 90-day average for these essentials, apply the Runway Formula:

Special note regarding inflation:

If your audited Burn Rate is $4,000 and you have $12,000 in a High-Yield Savings Account (HYSA), your runway is exactly 3.0 months. However, if utility or grocery costs rise by 10% (as tracked by the BLS Consumer Price Index), your $4,000 baseline effectively becomes $4,400– shrinking your runway to 2.7 months.

3. The Opportunity Cost of Idle Capital

A CFO’s job isn't just to save; it's to optimize. While your emergency fund must be liquid, it should not be "dead money."

The Yield Gap: If your fund sits in a standard checking account at 0.05% while 2026 HYSA rates are 4.25%, you are experiencing an "Efficiency Leak." On a $20,000 fund, that is an $840 annual loss in purchasing power.

The Quarterly Runway Audit (Worksheet)

Utilize this framework for your quarterly household review. A downloadable version is available for our Substack subscribers.

Join the Executive Summary

Stop guessing at your financial security.

Our mission is to provide the mathematical frameworks you need to lead your household with confidence. Join our Substack to receive the Executive Summary– our periodic briefing on shifting 2026 economic benchmarks and a downloadable Runway Audit Worksheet to keep your household's bottom line secure.

External links for more information on this topic:

Contact

Feedback, inquiries: hello@theveramath.com

© 2026 The Vera Math. All rights reserved.

Privacy Policy & Terms

Financial Disclaimer: The content on The Vera Math is for informational and educational purposes only and does not constitute professional financial, tax, or legal advice. I am a Household CFO sharing personal experience and math-based insights; please consult with a licensed professional before making significant financial decisions.