Where’s My Money? The 2026 IRS Refund Schedule and the CP53E Notice

Is your 2026 tax refund frozen? Find the official IRS refund schedule, PATH Act dates, and what Notice CP53E means for your bank account here.

TAX STRATEGY & UPDATES

Nyeva

2/12/20263 min read

If you’ve already hit “send” on your 2025 tax return, you’re likely refreshing the Where’s My Refund? tool daily. But this year, the “Where’s My Money” dance has a few new steps. Between the PATH Act and a major shift in how the IRS handles paper checks, your refund might be “frozen” even if you did everything right.

Here is exactly when you can expect your cash and what that mysterious CP53E notice actually means for your bank account.

The 2026 Refund Timeline: When Will It Hit?

For most early filers, the standard 21-day window still applies. However, if you claimed the Earned Income Tax Credit (EITC) or the Additional Child Tax Credit (ACTC), federal law requires the IRS to hold your entire refund until mid-February.

Key Dates for your 2026 Refund:

January 26, 2026: IRS begins processing.

February 16, 2026: The PATH Act hold is officially lifted.

February 21, 2026: The Where’s My Refund? tool will update with actual deposit dates for PATH Act filers.

February 27–March 2, 2026: The "Big Wave." This is the date the IRS expects most direct deposits to actually land in bank accounts.

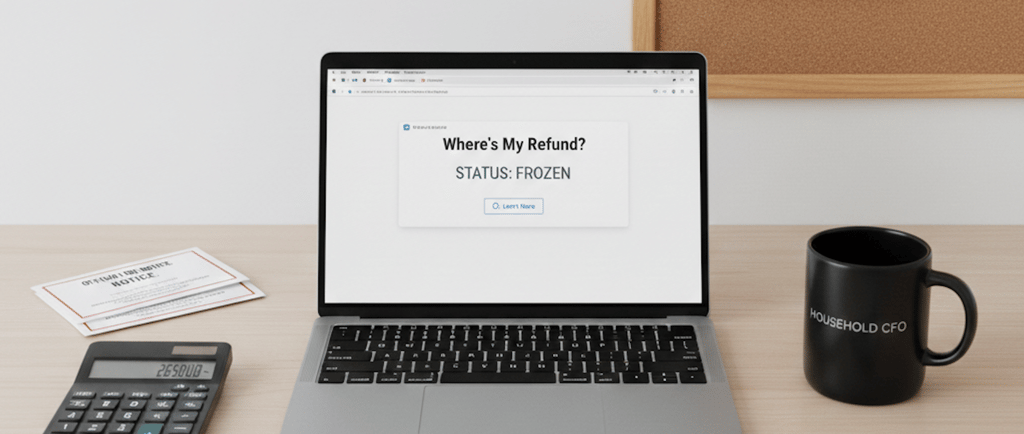

Why Is My Refund Frozen? Enter Notice CP53E

If you check your status and see a "Freeze," don't panic. Under Executive Order 14247, the IRS has officially begun phasing out paper refund checks.

If you didn’t provide bank account info, or if your bank rejected the deposit, the IRS will send you Notice CP53E.

What you need to know about the CP53E:

30-Day Window: You have 30 days to log into your IRS Online Account and provide valid direct deposit information.

The Six-Week Penalty: If you ignore the notice or can't provide a bank account, your refund moves to "manual processing." This triggers a minimum six-week delay before a paper check is mailed.

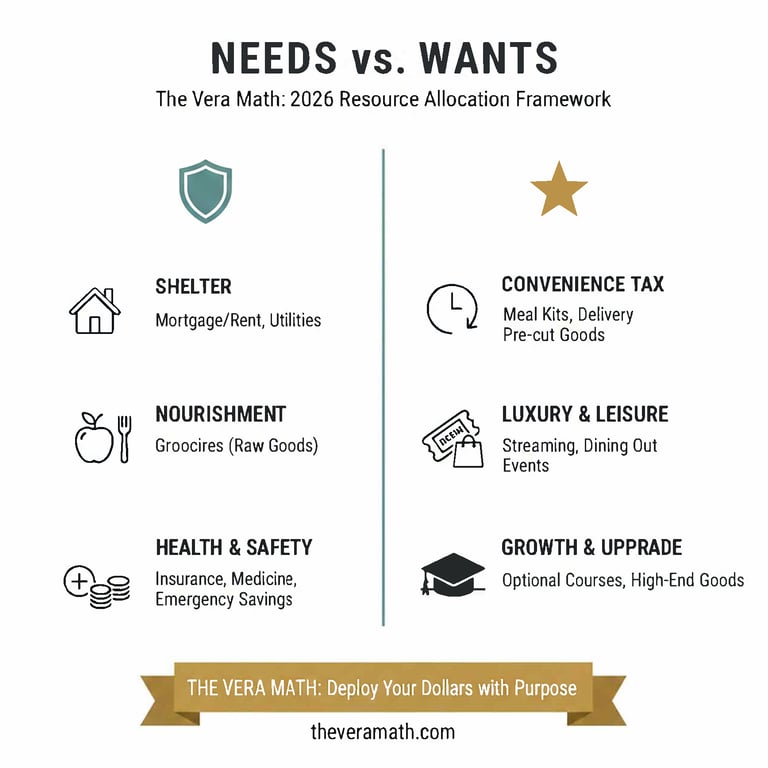

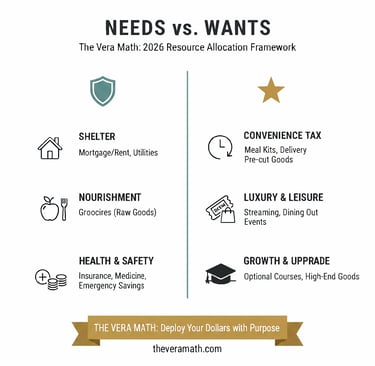

Strategic Spending: Staples vs. Wants

While you wait for that "Refund Sent" status to hit your bank account, now is the time to get your plan in place. A tax refund is essentially an injection of cash– the easiest way to get ahead of your bills and breathe a little easier for the rest of the year.

The Strategy: Staples First

As you can see in the chart above, the goal is to categorize your spending before you touch a single cent. In the high-inflation world of 2026, the best way to make your refund last is to focus on the things that actually keep your household running.

Nail Down the Basics: Your first priority should always be the "Needs" column. Think of this as "buying your peace of mind." Using your refund to create a buffer for utilities or putting a dent in your housing costs isn't just paying bills– it’s making sure your future self isn't stressed in six months.

Build Your Safety Net: If the basics are covered, look at your health costs and savings. These are the non-negotiables that protect you from life’s "what-ifs."

Handling the Fun Stuff: Only after those are secure should you look at the "Wants" column. Whether it’s a new gadget, a night out, or the convenience of a meal kit, these should only be funded by what’s left over.

A "Staple-First" strategy is the most practical way to ensure your refund actually does some work for you, rather than just disappearing into a few weeks of "convenience" spending.

How to Speed Up a "Frozen" Refund

Verify your ID.me: Ensure you can log into the IRS website before you get a notice.

Official Tools: You can check your status on the official IRS Where's My Refund tool.

Detailed Guidance: For a full breakdown of the freeze, see the IRS guide to Notice CP53E.

Join the Executive Summary

Want the TL;DR on tax season updates and financial strategy? Join our Substack to get the Executive Summary delivered straight to you inbox.

External links for more information on this topic:

Contact

Feedback, inquiries: hello@theveramath.com

© 2026 The Vera Math. All rights reserved.

Privacy Policy & Terms

Financial Disclaimer: The content on The Vera Math is for informational and educational purposes only and does not constitute professional financial, tax, or legal advice. I am a Household CFO sharing personal experience and math-based insights; please consult with a licensed professional before making significant financial decisions.